The largest oil producer in Africa keeps creating sovereign wealth funds and starving them. The outcome is a fiscal architecture that appears sophisticated on paper but collapses under the strain of political bargaining whenever crude prices spike.

Crude Reality

At peak output, Nigeria produces about 1.7 million barrels of crude per day, according to the Nigerian National Petroleum Company Limited, but the country has no meaningful war chest to show for it as global oil prices climb on the back of

The Nigeria Sovereign Investment Authority (NSIA), the country’s flagship savings vehicle, continues to accumulate assets, but at a rate that is nowhere near the scale of oil revenue coursing through Africa’s largest economy. Every price shock opens the old wound again: should windfall earnings be saved or shared immediately among federal, state, and local governments?

That question has been unanswered for two decades, and the cost is now structural.

From ECA to NSIA

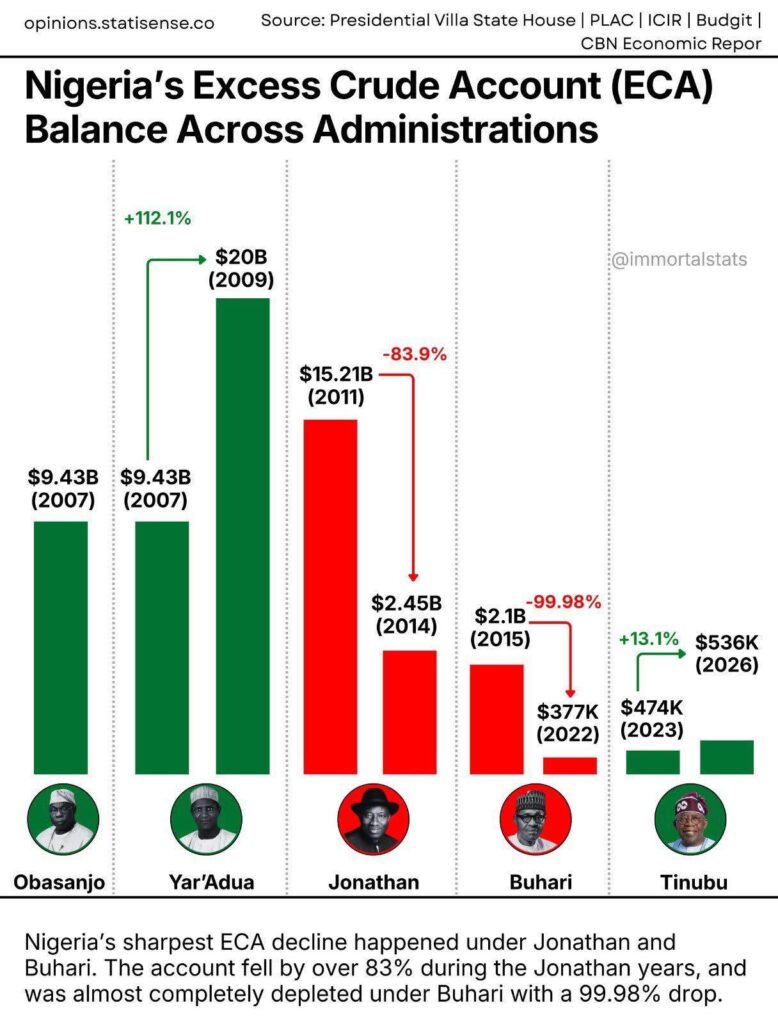

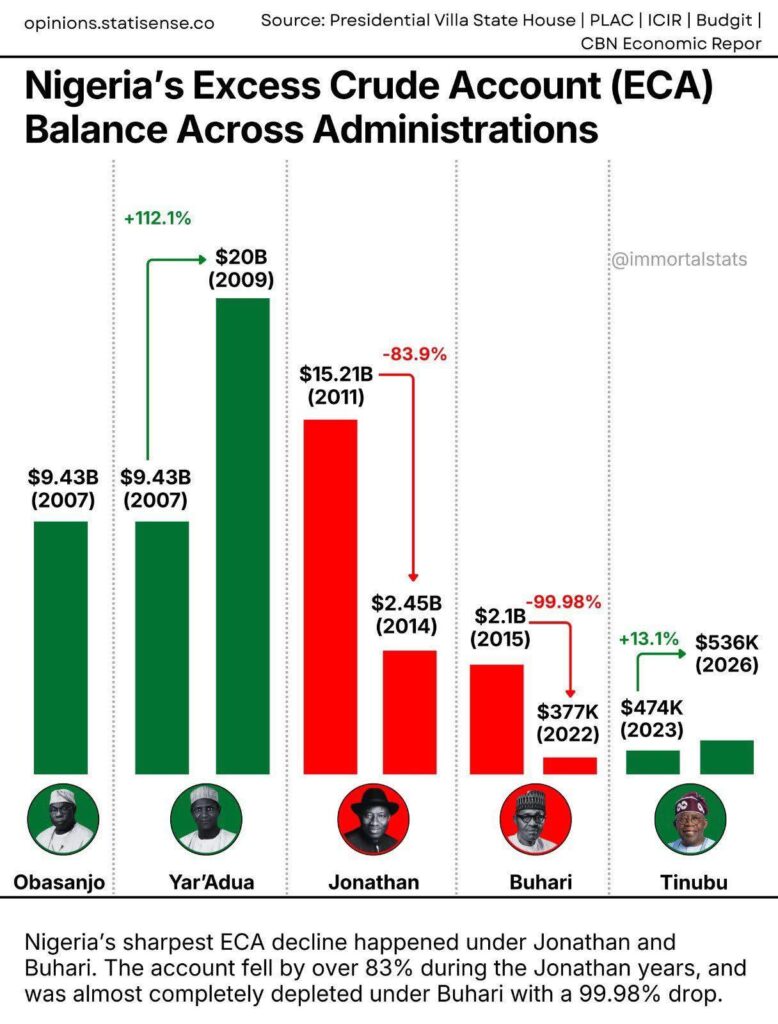

The story starts with the Excess Crude Account (ECA), established by President Olusegun Obasanjo and then Finance Minister Ngozi Okonjo-Iweala (now Director-General of the World Trade Organisation). The mechanism was beautifully simple – when crude sold above the benchmark price in Nigeria’s annual budget, the surplus would be saved.

The 36 state governors disagreed and took the federal government to court in 2008 and again in 2011, challenging Abuja’s authority to operate the ECA and to make unilateral deductions. The account never recovered.

Instead, the NSIA was established by law in 2011 and started operations in 2013. It was designed to do what the ECA could not: survive politics. The fund is divided into three windows – a stabilisation fund for budget shocks, a future generations fund for the post-oil period and an infrastructure fund to cover domestic development gaps.

By Nigerian standards, the NSIA has delivered. It has financed infrastructure projects, funded healthcare and agriculture initiatives and tapped global capital markets. But its assets are still dwarfed by Norway’s roughly $1.7 trillion Government Pension Fund Global, or the Gulf sovereign funds that now dictate the flow of global capital.

Abuja’s Gamble

Nigeria does not have a sovereign wealth problem. It has a sovereign consensus problem.

Arguably, the NSIA is one of the better-run institutions in Nigeria’s public finance ecosystem, but no institution, no matter how well managed, can outperform the political settlement it sits within. As long as governors see oil receipts as money that should go to the Federation Account for sharing, and the federal government lacks the political capital to impose a savings rule, the fund will be a symbolic rather than a fiscal vehicle.

This is the strategic gamble at the core of Nigerian fiscal policy: successive governments have opted for short-term political peace with the states over long-term fiscal insurance. Each time global oil prices crash or an IMF mission lands in Abuja with conditionalities, the bill for that choice comes.

The likely result is simply more of the same. Nigeria will keep alternating between saving and spending, the NSIA will keep growing modestly, and the country will keep facing each external shock with a near-empty stabilisation buffer. Until the federation agrees on a binding savings rule that the states themselves help to design, the trillion-dollar comparison with Norway will be a rhetorical device, not a roadmap.

The Other Side

Another view is that Nigeria’s peculiarities simply do not permit Norwegian-style discipline. With poverty at multi-decade highs, infrastructure deficits measured in the hundreds of billions of dollars, and over 130 million Nigerians classified as multidimensionally poor by the National Bureau of Statistics, immediate spending — even windfall revenues — may yield higher social returns than locking funds away for future generations. By this logic, the states are not being reckless; they are being responsive to a population that cannot afford to wait.

Notable

Sub-Saharan Africa’s other major oil producers are facing similar reckonings. Angola, the region’s second-largest crude exporter, has drawn heavily on its Fundo Soberano de Angola as its output has fallen and debt service costs have increased. Ghana, which began commercial oil production only in 2010, has tapped its Stabilisation Fund repeatedly to plug budget gaps during its recent IMF programme. The trend hints that for African petrostates, the sovereign wealth fund is increasingly serving less as a generational savings vehicle and more as a fiscal shock absorber of last resort.

The post Nigeria’s Trillion-Naira Savings Paradox appeared first on Latest Breaking News – News Central TV.